OnePoint Insurance Agency Blog

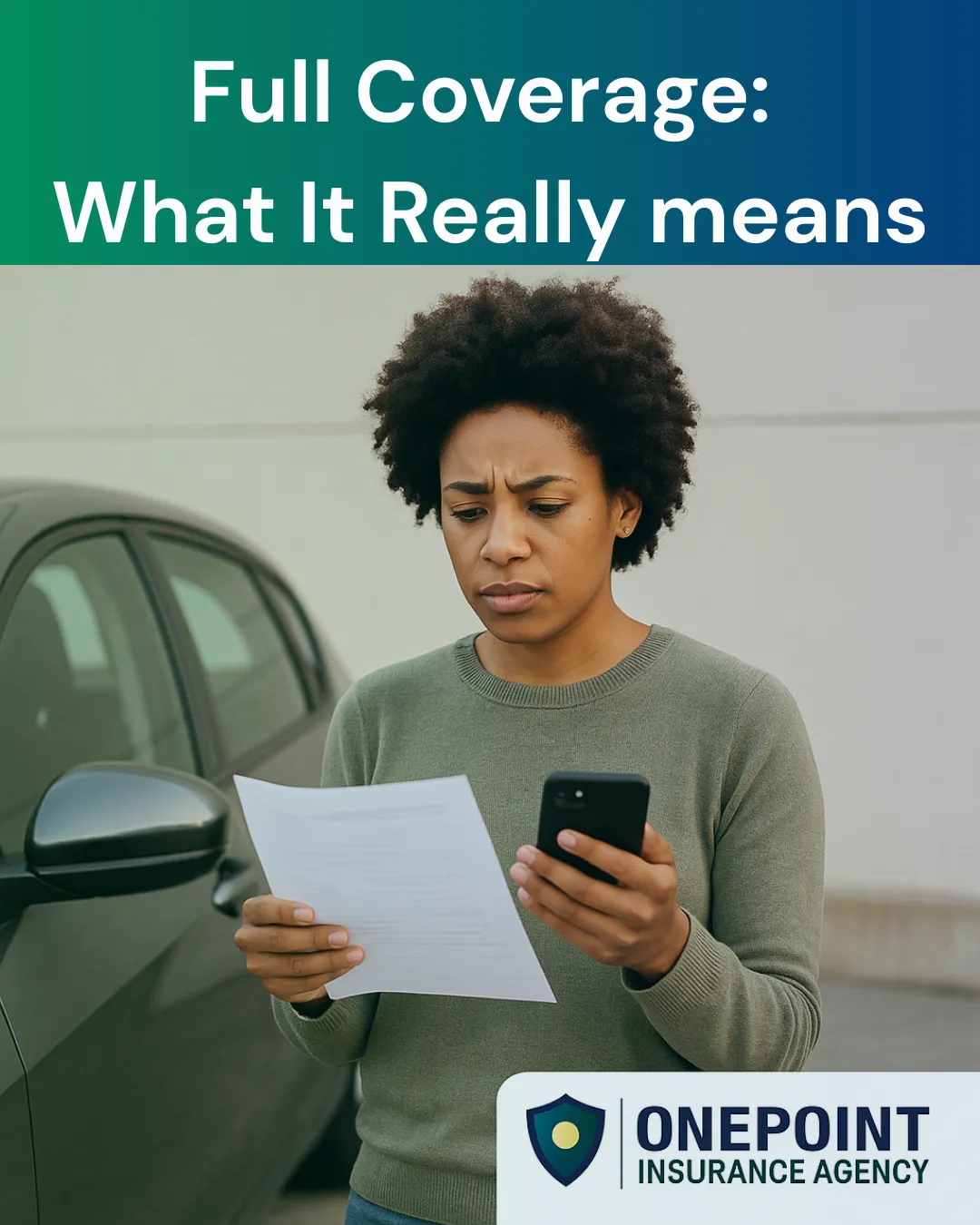

What Is Full Coverage Auto Insurance?

“They told me I had full coverage… until I needed it.”

Don’t let this be your story. Discover what full coverage really means—because when the unexpected happens, clarity beats assumptions every time.

The Myth of "Full Coverage"

If you've ever purchased car insurance, chances are you've heard the term “full coverage” thrown around. It sounds reassuring, doesn’t it?

Like a warm, invisible shield surrounding your car, ready to protect you from any disaster.

But here's the truth:

“Full coverage” is not an actual policy or standardized term in the insurance industry. It’s a misunderstood catchphrase—often overused and under-explained.

Most drivers think “full coverage” means total protection. Unfortunately, it’s a misleading phrase that can leave you dangerously exposed. At OnePoint Insurance Agency, we often meet clients in Georgia and Texas who believed they were covered—until a claim proved otherwise. Let’s break down:

What “full coverage” usually includes.

Common exclusions.

Must-have endorsements and add-ons (like glass coverage)

How to create a customized, real full coverage plan

Why bundling with OnePoint saves you time and money

What Does “Full Coverage” Typically Include?

“Full coverage” usually refers to a policy that bundles:

✅ Liability Insurance

Covers injuries or property damage you cause to others.

✅ Collision Coverage

Pays for damage to your car from a collision, regardless of fault

✅ Comprehensive Coverage

Protects against non-collision events:

Theft

Vandalism

Fire

Weather (hail, flood, wind)

Falling objects

Animal impacts (like hitting a deer)

These are great starting points—but still leave critical gaps in protection.

What’s Missing From "Full Coverage"?

Even with liability, collision, and comprehensive, many essential protections are not included unless you request them:

❌ Uninsured/Underinsured Motorist (UM/UIM)

❌ Personal Injury Protection (PIP) or Medical Payments (MedPay)

❌ Rental Car Reimbursement

❌ Roadside Assistance

❌ Gap Insurance

❌ OEM Parts Replacement

❌ Glass Coverage (Windshield/Windows)

Want a quick check to see if your policy includes these?

👉 Click here to review your options or get a quote now

🪟 What Is Glass Coverage — and Do You Need It?

Glass coverage is an often-overlooked endorsement that protects your:

Windshield

Side and rear windows

Sunroof or moonroof

In Georgia and Texas, replacing a windshield can cost $250 to $1,500 or more. Comprehensive may help — but only after you pay a deductible.

With a Full Glass Coverage Endorsement, repairs or replacements are often fully covered with no deductible.

If you commute daily, drive in high-construction zones, or live in hail-prone areas (like North Texas), this add-on is a must-have.

🔒 Common Auto Insurance Endorsements You Shouldn’t Ignore

To truly be “fully covered,” consider these policy endorsements that extend or enhance your protection:

Georgia and Texas-Specific Considerations

Georgia (GA):

Allows UM/UIM coverage stacking

High deer collision rate — glass & comp coverage recommended

Texas (TX):

High rate of uninsured drivers

Hail-prone areas like Dallas and Fort Worth demand stronger glass and comp coverage

State mandates PIP unless waived in writing

👀 Why "Full Coverage" Isn’t Enough in Real Life

Here’s a real-world scenario:

Your brand-new SUV gets sideswiped by an uninsured driver. Your insurance covers their damage—but your $1,500 windshield crack isn’t fully paid because you didn’t add zero-deductible glass coverage.

Sound familiar? Don’t let assumptions cost you thousands.

🛡 How to Get Real Full Coverage with OnePoint Insurance

At OnePoint Insurance Agency, we build custom, comprehensive auto policies tailored to your lifestyle—not cookie-cutter plans.

Why Georgia & Texas Drivers Choose OnePoint:

✓ Fast, affordable online quotes

✓ Same-day coverage available

✓ Experts in commercial & personal auto

✓ Local agents who understand your state laws

✓ Bilingual support available

👉 Click here to build your real full coverage plan now

🎯 Get a Personalized Auto Insurance Quote Today

Ready to upgrade to real full coverage?

✅ Protect every part of your vehicle

✅ Get peace of mind for your family

✅ Backed by a trusted local agency

Start now:

➡️ Get an auto insurance quote today.

➡️ Available in Georgia & Texas

📞 Ready to build a real full coverage plan?

👉 Call us at 770-884-8117 or click here to schedule your policy review

What Is Full Coverage Auto Insurance?

“They told me I had full coverage… until I needed it.”

Don’t let this be your story. Discover what full coverage really means—because when the unexpected happens, clarity beats assumptions every time.

The Myth of "Full Coverage"

If you've ever purchased car insurance, chances are you've heard the term “full coverage” thrown around. It sounds reassuring, doesn’t it?

Like a warm, invisible shield surrounding your car, ready to protect you from any disaster.

But here's the truth:

“Full coverage” is not an actual policy or standardized term in the insurance industry. It’s a misunderstood catchphrase—often overused and under-explained.

Most drivers think “full coverage” means total protection. Unfortunately, it’s a misleading phrase that can leave you dangerously exposed. At OnePoint Insurance Agency, we often meet clients in Georgia and Texas who believed they were covered—until a claim proved otherwise. Let’s break down:

What “full coverage” usually includes.

Common exclusions.

Must-have endorsements and add-ons (like glass coverage)

How to create a customized, real full coverage plan

Why bundling with OnePoint saves you time and money

What Does “Full Coverage” Typically Include?

“Full coverage” usually refers to a policy that bundles:

✅ Liability Insurance

Covers injuries or property damage you cause to others.

✅ Collision Coverage

Pays for damage to your car from a collision, regardless of fault

✅ Comprehensive Coverage

Protects against non-collision events:

Theft

Vandalism

Fire

Weather (hail, flood, wind)

Falling objects

Animal impacts (like hitting a deer)

These are great starting points—but still leave critical gaps in protection.

What’s Missing From "Full Coverage"?

Even with liability, collision, and comprehensive, many essential protections are not included unless you request them:

❌ Uninsured/Underinsured Motorist (UM/UIM)

❌ Personal Injury Protection (PIP) or Medical Payments (MedPay)

❌ Rental Car Reimbursement

❌ Roadside Assistance

❌ Gap Insurance

❌ OEM Parts Replacement

❌ Glass Coverage (Windshield/Windows)

Want a quick check to see if your policy includes these?

👉 Click here to review your options or get a quote now

🪟 What Is Glass Coverage — and Do You Need It?

Glass coverage is an often-overlooked endorsement that protects your:

Windshield

Side and rear windows

Sunroof or moonroof

In Georgia and Texas, replacing a windshield can cost $250 to $1,500 or more. Comprehensive may help — but only after you pay a deductible.

With a Full Glass Coverage Endorsement, repairs or replacements are often fully covered with no deductible.

If you commute daily, drive in high-construction zones, or live in hail-prone areas (like North Texas), this add-on is a must-have.

🔒 Common Auto Insurance Endorsements You Shouldn’t Ignore

To truly be “fully covered,” consider these policy endorsements that extend or enhance your protection:

Georgia and Texas-Specific Considerations

Georgia (GA):

Allows UM/UIM coverage stacking

High deer collision rate — glass & comp coverage recommended

Texas (TX):

High rate of uninsured drivers

Hail-prone areas like Dallas and Fort Worth demand stronger glass and comp coverage

State mandates PIP unless waived in writing

👀 Why "Full Coverage" Isn’t Enough in Real Life

Here’s a real-world scenario:

Your brand-new SUV gets sideswiped by an uninsured driver. Your insurance covers their damage—but your $1,500 windshield crack isn’t fully paid because you didn’t add zero-deductible glass coverage.

Sound familiar? Don’t let assumptions cost you thousands.

🛡 How to Get Real Full Coverage with OnePoint Insurance

At OnePoint Insurance Agency, we build custom, comprehensive auto policies tailored to your lifestyle—not cookie-cutter plans.

Why Georgia & Texas Drivers Choose OnePoint:

✓ Fast, affordable online quotes

✓ Same-day coverage available

✓ Experts in commercial & personal auto

✓ Local agents who understand your state laws

✓ Bilingual support available

👉 Click here to build your real full coverage plan now

🎯 Get a Personalized Auto Insurance Quote Today

Ready to upgrade to real full coverage?

✅ Protect every part of your vehicle

✅ Get peace of mind for your family

✅ Backed by a trusted local agency

Start now:

➡️ Get an auto insurance quote today.

➡️ Available in Georgia & Texas

📞 Ready to build a real full coverage plan?

👉 Call us at 770-884-8117 or click here to schedule your policy review

What Is Full Coverage Auto Insurance?

“They told me I had full coverage… until I needed it.”

Don’t let this be your story. Discover what full coverage really means—because when the unexpected happens, clarity beats assumptions every time.

The Myth of "Full Coverage"

If you've ever purchased car insurance, chances are you've heard the term “full coverage” thrown around. It sounds reassuring, doesn’t it?

Like a warm, invisible shield surrounding your car, ready to protect you from any disaster.

But here's the truth:

“Full coverage” is not an actual policy or standardized term in the insurance industry. It’s a misunderstood catchphrase—often overused and under-explained.

Most drivers think “full coverage” means total protection. Unfortunately, it’s a misleading phrase that can leave you dangerously exposed. At OnePoint Insurance Agency, we often meet clients in Georgia and Texas who believed they were covered—until a claim proved otherwise. Let’s break down:

What “full coverage” usually includes.

Common exclusions.

Must-have endorsements and add-ons (like glass coverage)

How to create a customized, real full coverage plan

Why bundling with OnePoint saves you time and money

What Does “Full Coverage” Typically Include?

“Full coverage” usually refers to a policy that bundles:

✅ Liability Insurance

Covers injuries or property damage you cause to others.

✅ Collision Coverage

Pays for damage to your car from a collision, regardless of fault

✅ Comprehensive Coverage

Protects against non-collision events:

Theft

Vandalism

Fire

Weather (hail, flood, wind)

Falling objects

Animal impacts (like hitting a deer)

These are great starting points—but still leave critical gaps in protection.

What’s Missing From "Full Coverage"?

Even with liability, collision, and comprehensive, many essential protections are not included unless you request them:

❌ Uninsured/Underinsured Motorist (UM/UIM)

❌ Personal Injury Protection (PIP) or Medical Payments (MedPay)

❌ Rental Car Reimbursement

❌ Roadside Assistance

❌ Gap Insurance

❌ OEM Parts Replacement

❌ Glass Coverage (Windshield/Windows)

Want a quick check to see if your policy includes these?

👉 Click here to review your options or get a quote now

🪟 What Is Glass Coverage — and Do You Need It?

Glass coverage is an often-overlooked endorsement that protects your:

Windshield

Side and rear windows

Sunroof or moonroof

In Georgia and Texas, replacing a windshield can cost $250 to $1,500 or more. Comprehensive may help — but only after you pay a deductible.

With a Full Glass Coverage Endorsement, repairs or replacements are often fully covered with no deductible.

If you commute daily, drive in high-construction zones, or live in hail-prone areas (like North Texas), this add-on is a must-have.

🔒 Common Auto Insurance Endorsements You Shouldn’t Ignore

To truly be “fully covered,” consider these policy endorsements that extend or enhance your protection:

Georgia and Texas-Specific Considerations

Georgia (GA):

Allows UM/UIM coverage stacking

High deer collision rate — glass & comp coverage recommended

Texas (TX):

High rate of uninsured drivers

Hail-prone areas like Dallas and Fort Worth demand stronger glass and comp coverage

State mandates PIP unless waived in writing

👀 Why "Full Coverage" Isn’t Enough in Real Life

Here’s a real-world scenario:

Your brand-new SUV gets sideswiped by an uninsured driver. Your insurance covers their damage—but your $1,500 windshield crack isn’t fully paid because you didn’t add zero-deductible glass coverage.

Sound familiar? Don’t let assumptions cost you thousands.

🛡 How to Get Real Full Coverage with OnePoint Insurance

At OnePoint Insurance Agency, we build custom, comprehensive auto policies tailored to your lifestyle—not cookie-cutter plans.

Why Georgia & Texas Drivers Choose OnePoint:

✓ Fast, affordable online quotes

✓ Same-day coverage available

✓ Experts in commercial & personal auto

✓ Local agents who understand your state laws

✓ Bilingual support available

👉 Click here to build your real full coverage plan now

🎯 Get a Personalized Auto Insurance Quote Today

Ready to upgrade to real full coverage?

✅ Protect every part of your vehicle

✅ Get peace of mind for your family

✅ Backed by a trusted local agency

Start now:

➡️ Get an auto insurance quote today.

➡️ Available in Georgia & Texas

📞 Ready to build a real full coverage plan?

👉 Call us at 770-884-8117 or click here to schedule your policy review

What Is Full Coverage Auto Insurance?

“They told me I had full coverage… until I needed it.”

Don’t let this be your story. Discover what full coverage really means—because when the unexpected happens, clarity beats assumptions every time.

The Myth of "Full Coverage"

If you've ever purchased car insurance, chances are you've heard the term “full coverage” thrown around. It sounds reassuring, doesn’t it?

Like a warm, invisible shield surrounding your car, ready to protect you from any disaster.

But here's the truth:

“Full coverage” is not an actual policy or standardized term in the insurance industry. It’s a misunderstood catchphrase—often overused and under-explained.

Most drivers think “full coverage” means total protection. Unfortunately, it’s a misleading phrase that can leave you dangerously exposed. At OnePoint Insurance Agency, we often meet clients in Georgia and Texas who believed they were covered—until a claim proved otherwise. Let’s break down:

What “full coverage” usually includes.

Common exclusions.

Must-have endorsements and add-ons (like glass coverage)

How to create a customized, real full coverage plan

Why bundling with OnePoint saves you time and money

What Does “Full Coverage” Typically Include?

“Full coverage” usually refers to a policy that bundles:

✅ Liability Insurance

Covers injuries or property damage you cause to others.

✅ Collision Coverage

Pays for damage to your car from a collision, regardless of fault

✅ Comprehensive Coverage

Protects against non-collision events:

Theft

Vandalism

Fire

Weather (hail, flood, wind)

Falling objects

Animal impacts (like hitting a deer)

These are great starting points—but still leave critical gaps in protection.

What’s Missing From "Full Coverage"?

Even with liability, collision, and comprehensive, many essential protections are not included unless you request them:

❌ Uninsured/Underinsured Motorist (UM/UIM)

❌ Personal Injury Protection (PIP) or Medical Payments (MedPay)

❌ Rental Car Reimbursement

❌ Roadside Assistance

❌ Gap Insurance

❌ OEM Parts Replacement

❌ Glass Coverage (Windshield/Windows)

Want a quick check to see if your policy includes these?

👉 Click here to review your options or get a quote now

🪟 What Is Glass Coverage — and Do You Need It?

Glass coverage is an often-overlooked endorsement that protects your:

Windshield

Side and rear windows

Sunroof or moonroof

In Georgia and Texas, replacing a windshield can cost $250 to $1,500 or more. Comprehensive may help — but only after you pay a deductible.

With a Full Glass Coverage Endorsement, repairs or replacements are often fully covered with no deductible.

If you commute daily, drive in high-construction zones, or live in hail-prone areas (like North Texas), this add-on is a must-have.

🔒 Common Auto Insurance Endorsements You Shouldn’t Ignore

To truly be “fully covered,” consider these policy endorsements that extend or enhance your protection:

Georgia and Texas-Specific Considerations

Georgia (GA):

Allows UM/UIM coverage stacking

High deer collision rate — glass & comp coverage recommended

Texas (TX):

High rate of uninsured drivers

Hail-prone areas like Dallas and Fort Worth demand stronger glass and comp coverage

State mandates PIP unless waived in writing

👀 Why "Full Coverage" Isn’t Enough in Real Life

Here’s a real-world scenario:

Your brand-new SUV gets sideswiped by an uninsured driver. Your insurance covers their damage—but your $1,500 windshield crack isn’t fully paid because you didn’t add zero-deductible glass coverage.

Sound familiar? Don’t let assumptions cost you thousands.

🛡 How to Get Real Full Coverage with OnePoint Insurance

At OnePoint Insurance Agency, we build custom, comprehensive auto policies tailored to your lifestyle—not cookie-cutter plans.

Why Georgia & Texas Drivers Choose OnePoint:

✓ Fast, affordable online quotes

✓ Same-day coverage available

✓ Experts in commercial & personal auto

✓ Local agents who understand your state laws

✓ Bilingual support available

👉 Click here to build your real full coverage plan now

🎯 Get a Personalized Auto Insurance Quote Today

Ready to upgrade to real full coverage?

✅ Protect every part of your vehicle

✅ Get peace of mind for your family

✅ Backed by a trusted local agency

Start now:

➡️ Get an auto insurance quote today.

➡️ Available in Georgia & Texas

📞 Ready to build a real full coverage plan?

👉 Call us at 770-884-8117 or click here to schedule your policy review

Address

555 North Point Center E Suite 400, Alpharetta, GA 30022

Phone No.

770-884-8117

Fax

770-884-8117

Social media

Legal

Privacy policy

Terms and conditions

©Copyright | OnePoint Insurance Agency. All Right Reserved

Information

About Us

Blog

©Copyright | OnePoint Insurance Agency. All Right Reserved